In construction, “bonding” and “insurance” are often talked about in the same breath. Many people assume they are interchangeable. They are not, and misunderstanding the difference can limit the type of work a contractor can pursue or expose a business to unnecessary risk.

Both surety bonds and insurance are critical tools for mid‑market construction companies. They are often required on the same project, but they exist for very different reasons. Understanding how each one works helps contractors qualify for better projects, meet owner requirements, and protect their businesses as they grow.

Why People Confuse Surety Bonds and Insurance

The confusion usually comes down to a basic misunderstanding of what each product is designed to do.

At a fundamental level:

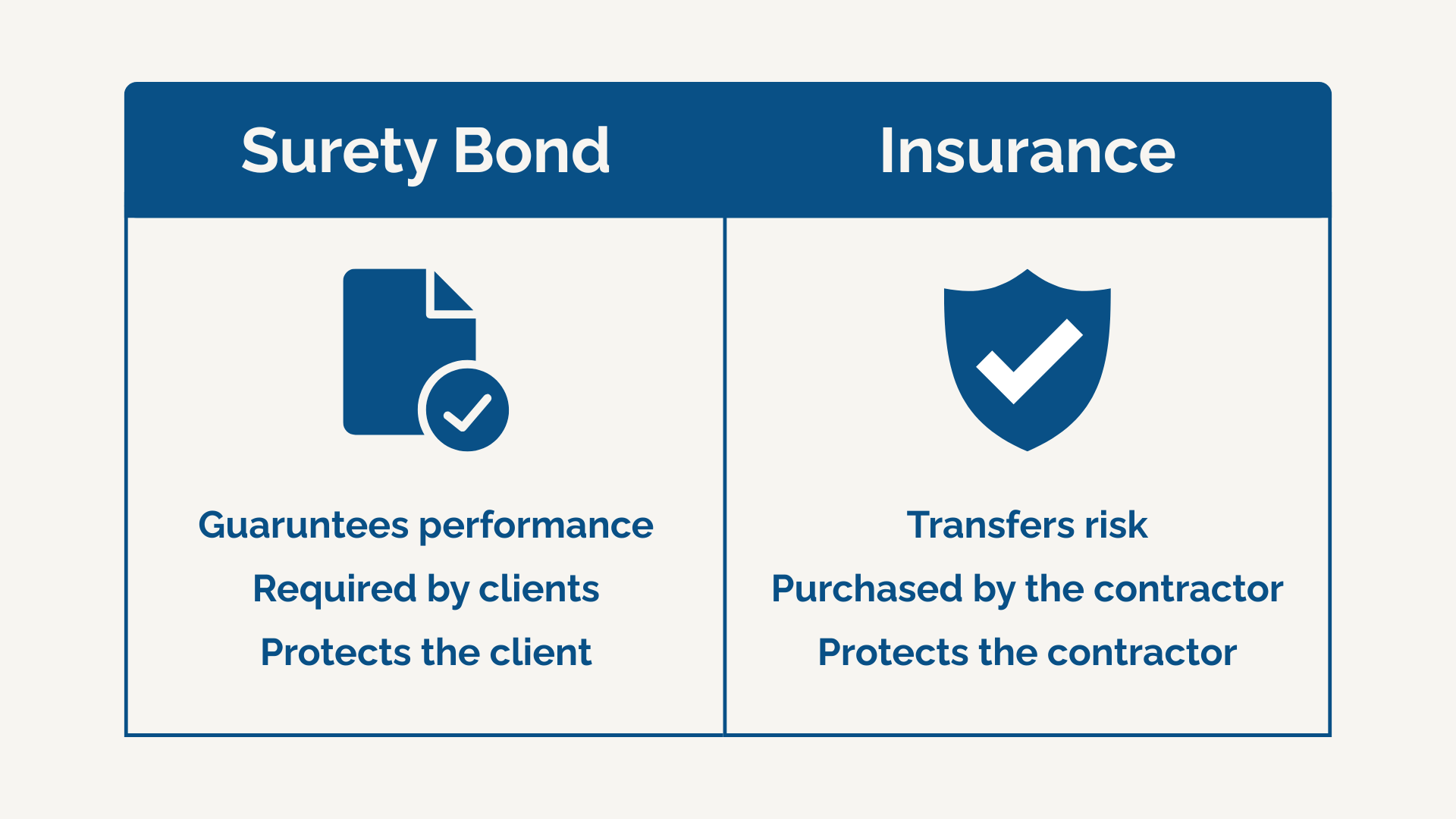

- Insurance transfers risk

- Surety guarantees completion

The difference becomes much clearer when you look at real‑world scenarios.

Insurance Example

A water leak causes damage to a building. The contractor has a valid insurance policy that covers this type of loss. The risk of that water damage was transferred to the insurance company, and the insurer pays the claim according to the policy terms.

This is insurance working exactly as intended. The contractor experiences a loss, and the insurer absorbs it.

Surety Example

A contractor is hired to build a community centre. During the project, the contractor makes construction and design errors, mismanages finances, and eventually goes bankrupt before finishing the job.

In this situation, the surety steps in to ensure the project is completed. The surety may finance the existing contractor, arrange for another contractor to finish the work, or complete the project directly.

The key point is this:

The surety’s obligation is to the project owner, not the contractor.

Key Differences Between a Surety Bond and Insurance

Rather than repeating a full technical comparison here, it is helpful to focus on the core distinction contractors need to understand:

- Insurance protects the contractor from loss

- Surety bonds protect the owner by guaranteeing performance

With insurance, the insurer expects claims to happen. With surety, claims are not expected, and the contractor is ultimately responsible for reimbursing the surety if a claim is paid.

If you want a deeper breakdown of how bonding works, this is covered in more detail in our construction bonding guide.

When You Need Each One

When Surety Bonds Are Required

You generally need a surety bond when the party hiring you requires it.

This is most common on:

- Municipal projects

- Provincial or federal work

- Public infrastructure projects

- Large institutional or corporate developments

For example, when a municipality is building a new school, it will typically require:

- A bid bond

- A performance bond

- A labour and material payment bond

In many cases, municipal projects over $500,000, and sometimes well under that amount, require bonding by default.

When Insurance Is Required

Insurance applies whenever a contractor faces potential financial loss.

This includes exposure from:

- Property damage

- Bodily injury

- Construction defects

- Professional errors

- Project‑specific risks such as builder’s risk or wrap‑ups

Every contractor should carry insurance, yet many are underinsured relative to their actual exposure. Industry experience shows that a large percentage of businesses do not carry enough coverage for the risks they assume.

Insurance ultimately comes down to risk tolerance. The real question is how much loss a contractor is willing, or able, to absorb themselves.

On many job sites, proof of insurance is mandatory before any work begins. In some cases, contractors are also required to carry specific limits or participate in project‑wide insurance programs.

How Bonding and Insurance Work Together

Bonding and insurance are often used at the same time, and in some cases, their coverage overlaps.

For example:

- A project is bonded with performance and payment bonds

- Each contractor carries general liability insurance

- The general contractor maintains wrap‑up liability coverage

- The project has a builder’s risk policy in place

Each layer addresses a different type of risk. Together, they create a more complete risk management structure for complex construction projects.

Common Construction Industry Examples

Surety bonds are most commonly required on:

- Municipal and public sector projects

- Infrastructure and civil construction

- Institutional work such as hospitals and schools

- Large private or corporate developments

Even when bonds are not legally required, many owners still insist on them to protect timelines, budgets, and subcontractors.

How Surety Bonds Benefit Contractors

Although surety bonds are designed to protect owners, they offer meaningful benefits to contractors as well.

Being bondable helps contractors:

- Qualify for larger and public projects

- Build credibility with owners, lenders, and partners

- Demonstrate financial and operational strength

- Compete more effectively in bid situations

- Establish long‑term trust in the marketplace

From an owner’s perspective, a bondable contractor signals stability and professionalism. From a contractor’s perspective, bonding opens doors that would otherwise remain closed.

Final Thoughts

Insurance and surety bonds are both essential, but they are not interchangeable.

Insurance protects your business from loss.

Surety bonds guarantee that you will meet your contractual obligations.

Understanding how each one works, and when it is required, puts contractors in a stronger position to grow, bid confidently, and manage risk effectively.

If you are unsure whether your current insurance or bonding program supports the type of work you want to pursue, it is often worth reviewing it before the next opportunity arises.

Contact us today to find out what the Buildsure program can do for you.